Investment Thesis

Thermo Fisher Scientific (NYSE: TMO) is well positioned to maintain its leadership in the global life sciences and healthcare tools market through its diversified presence across four major business segments: Life Sciences Solutions, Analytical Instruments, Specialty Diagnostics, and Biopharma Services.

This breadth enables the company to capture secular growth trends in genomics, biologics outsourcing, and predictive diagnostics while mitigating volatility in any single market segment. TMO’s consistent ability to generate strong free cash flow (around $6.8B and projected to exceed $10 billion by 2029 in a base case) combined with stabilizing gross margins around 42%, provide a solid foundation for shareholder returns and continued reinvestment in innovation.

While the stock currently trades at a modest premium to intrinsic value, the potential for portfolio optimization, particularly through the divestiture of lower-growth diagnostics units, as well as upcoming product launches in proteomics and AI-driven lab automation, create catalysts that may not yet be fully appreciated by the market. The company’s expanding CDMO platform further enhances long-term growth prospects, though near-term valuation suggests a balanced risk-reward profile best suited for a Hold recommendation.

Company Overview

Thermo Fisher Scientific operates a highly diversified business model that spans instruments, consumables, diagnostics, and contract services. Its broad customer base includes pharmaceutical and biotechnology companies, hospitals and clinical laboratories, academic institutions, and government agencies, reflecting the company’s role as an essential partner across the global scientific ecosystem. In 2024, TMO generated $42 billion in revenue from operations in more than 50 countries, underscoring its scale and geographic reach.

The company was established in 2006 through the merger of Thermo Electron and Fisher Scientific, a combination that created a global leader in scientific products and services. Since then, TMO has expanded significantly through targeted acquisitions, including Life Technologies in 2014 to strengthen its genomics and molecular biology capabilities, Patheon in 2017 to enhance its biopharma services, and PPD in 2021 to build out its clinical research and contract development expertise. These acquisitions reflect the company’s strategy of extending its value chain from early-stage research through clinical development and commercial manufacturing.

Today, TMO operates through four primary business segments: Life Sciences Solutions, Analytical Instruments, Specialty Diagnostics, and Laboratory Products & Biopharma Services. This segmentation not only provides a balanced revenue mix but also creates opportunities for cross-segment integration and customer retention. The company’s competitive edge lies in its position as a true “one-stop shop” for scientific research and biopharma production. With integrated offerings that combine R&D tools and CDMO services, Thermo Fisher delivers unmatched scale and efficiency, while proprietary platforms such as the Gibco Cell Therapy Systems (CTS) and the Ion Torrent sequencing portfolio further reinforce its technological leadership.

Industry & Market Analysis

Thermo Fisher operates in high-growth segments of the life sciences industry. Genomics and predictive biomarkers are expanding at ~19% CAGR, diagnostics at ~29%, analytical instruments at ~6%, and CDMO/lab supplies at ~8%. These trends highlight strong secular demand, particularly in precision medicine, decentralized testing, and outsourced manufacturing.

Competition remains intense. Diversified peers like Danaher and Agilent, along with niche players such as Bruker and Bio-Rad, drive high industry rivalry. Buyer power is significant for large pharma clients, while entry barriers are high due to capital intensity and regulation. Substitution risk is limited in advanced tools like proteomics but more pronounced in commoditized consumables.

Macro and regulatory factors present both risks and opportunities. NIH budget cuts, Medicare reimbursement reform, and weak Chinese hospital spending weigh on near-term demand. Yet aging populations, rising chronic disease, and adoption of AI/ML in labs provide long-term structural tailwinds that align closely with Thermo Fisher’s portfolio.

Financial Valuation and Return Potential

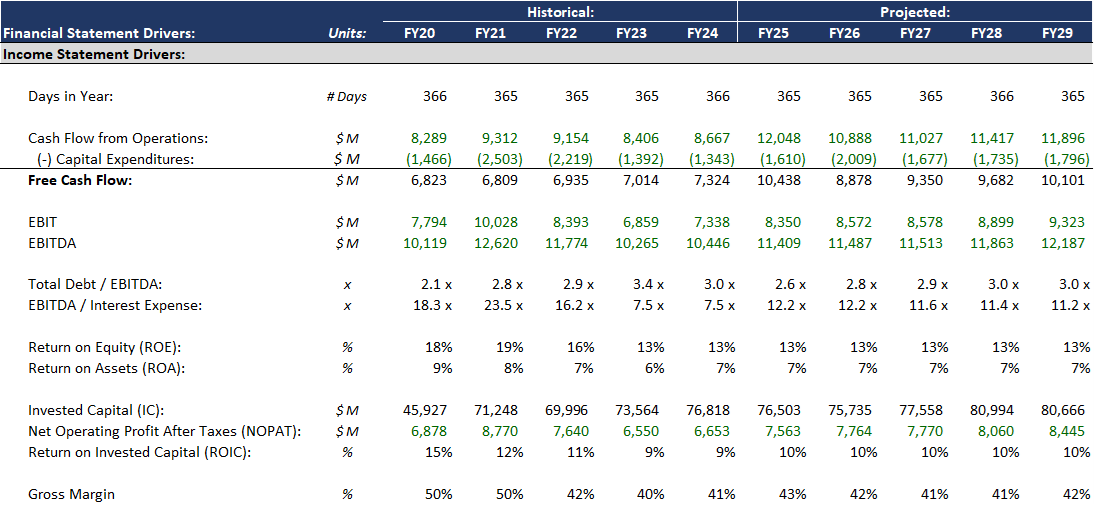

To forecast the three-statement model (income statement, balance sheet and cash flow statement) for the DCF valuation, historical averages were primarily used, with several key assumptions applied. First, revenue projections were based on previous research into the company’s four operating segments, with respective annual growth rates of approximately 6%, 7%, 2%, and 4% for the four business units separately. Second, COGS, operating expenses, interest expense, and the effective tax rate were estimated using either historical trends or multi-year averages. Third, operating balance sheet items, including accounts receivable, accounts payable, accrued expenses, contract assets, and contract liabilities, were modeled based on five-year averages, reflecting the company’s maturity and historically steady performance. Fourth, other critical elements such as deferred tax liabilities, dividend payouts, and total debt were projected using income or asset benchmarks (e.g., dividends as a fixed percentage of net income), consistent with operational norms and sustainable financial management practices. Finally, projections for capital expenditures and acquisitions, along with the resulting depreciation schedule and asset base, were derived through a more nuanced asset allocation model. The detailed methodology and calculations can be found in the accompanying Excel model.

Based on the three statements, several key ratios are worth mentioning. Thermo Fisher has averaged revenue growth of roughly 8% annually from 2020 to 2024 and gross margins stabilizing near 43%. Earnings were pressured in recent years by foreign exchange volatility and acquisition integration costs but are now rebounding. Profitability remains solid, with return on equity around 16% and return on invested capital projected around 11%. Free cash flow has consistently exceeded $6.5 billion and is expected to surpass $10 billion by the end of the decade, supporting both reinvestment and shareholder returns.

The balance sheet shows a manageable leverage profile. Net debt to EBITDA peaked at 3.4x in 2023 but is trending down toward 2.6–3.0x, while interest coverage has remained steadily above 7.5x, reflecting stronger earnings capacity.

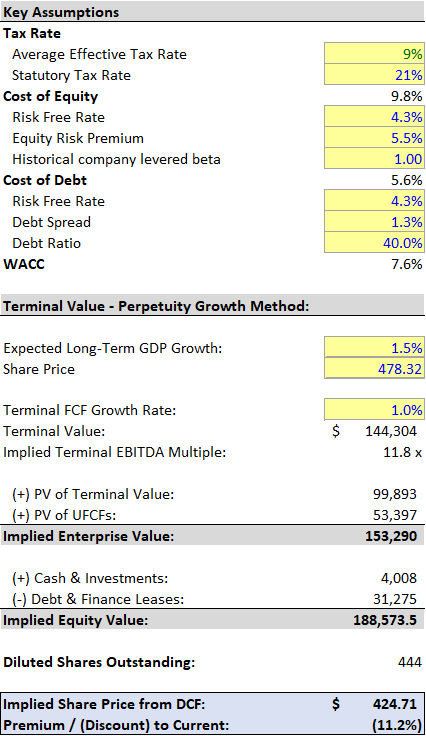

In the DCF model, the base case yields an implied enterprise value of $153.3 billion and an implied equity value of $188.6 billion. With 444 million diluted shares outstanding, the model results in a DCF-derived share price of $424.71, representing an 11.2% discount compared to the current market price of $478.32. This suggests that, under conservative assumptions (including a 1.0% terminal FCF growth rate and an 11.8x terminal EBITDA multiple), TMO may be modestly overvalued by the market. However, its strong cash flow generation and strategic positioning keep the intrinsic value within a reasonable range of the trading price.

Of course, this outcome is only one possible result based on a set of rational assumptions. To evaluate how sensitive this valuation is to key financial variables, scenario and sensitivity analyses are used. These tools are especially useful in highlighting how valuation shifts when certain financial levers are pulled in different directions.

The four variables tested in this section include: 1) Discount rate (WACC), 2) Revenue growth, 3) Gross margin assumptions and 4) Terminal FCF growth rate.

For revenue growth assumptions, in the base case, a weighted average revenue growth rate of ~3% was assumed over five years. If revenue growth increases to 10%, the implied valuation rises to $465.18 per share, only 2.7% below the current market price, suggesting near parity. On the other hand, if growth drops to 1%, the implied value decreases to $410.04. This implies that while revenue growth does influence valuation, the changes are moderate unless paired with other drivers. For gross margin, an optimistic scenario assumes product margins increase to 55% and service margins to 32%, in line with historical peaks. Under this assumption, the implied share price rises to $475.31—virtually equal to the current market value. This shows that even modest cost optimization in product manufacturing could enhance value more than a large increase in topline growth.

Moving on to the sensitivity analysis, the terminal FCF growth rate and discount rate assumption is particularly influential. In the base case, it is set at 1.0%, slightly below the U.S. long-term GDP forecast of 1.5%. Importantly, this rate should not exceed GDP growth over the long term, as doing so would imply the company eventually outgrows the entire economy—an unrealistic scenario (Brealey et al., 2020). A sensitivity matrix plotting share price against different combinations of WACC and terminal growth rates reveals that small changes in either variable can have a disproportionate impact on valuation. This reinforces the importance of operational initiatives that increase perceived long-term growth and reduce business risk.

In summary, the most critical variables affecting valuation include revenue growth, cost structure, discount rate, and terminal growth expectations. Because TMO is a mature and stable company, no single factor drastically changes its valuation. However, when several variables shift in tandem, the impact on intrinsic value can be significant.

Please note that this analysis relies solely on the DCF with a perpetuity growth model. Alternative approaches such as comparable company analysis or a DCF with exit multiples could be applied to validate and cross-check the results.

Catalysts and Risks

Several upcoming developments could serve as meaningful catalysts for Thermo Fisher Scientific’s stock performance. The planned divestiture of lower-growth diagnostics units in 2025 should allow the company to reallocate capital toward higher-margin and faster-growing areas, sharpening its strategic focus. New product launches in proteomics, single-cell analysis, and AI-driven lab automation are expected to enhance the company’s innovation leadership and expand addressable markets. In addition, Thermo Fisher’s contract development and manufacturing (CDMO) and bioproduction services are poised for growth as biotech funding rebounds, supporting increased demand for outsourced solutions. Finally, the company retains the flexibility to pursue bolt-on acquisitions in high-growth verticals, further strengthening its competitive position and broadening its portfolio.

Despite its strong positioning, Thermo Fisher faces notable risks that could impact future performance. On a company-specific level, its acquisition-heavy growth strategy carries ongoing integration challenges, with $45 billion in goodwill and $14 billion in intangible assets creating potential impairment risk if synergies fall short. Customer concentration among large pharmaceutical firms also heightens pricing and negotiation pressures, while foreign exchange volatility poses recurring headwinds. At the industry level, competition remains intense across instruments, diagnostics, and CDMO services, with rivals and large buyers exerting downward pricing pressure. On the macro front, reductions in R&D budgets in the United States and China, continued reimbursement reforms, and the potential for rising interest rates to elevate the company’s cost of capital all represent external threats that could weigh on profitability and valuation.

Recommendation

Thermo Fisher Scientific warrants a Hold rating, reflecting a balanced risk-reward profile at its current valuation. While the company is financially strong and strategically well-positioned, trading at a modest premium to intrinsic value limits near-term upside. For portfolio construction, the stock is best suited as a core defensive healthcare holding. Over a three- to five-year horizon, Thermo Fisher’s consistent free cash flow generation and stabilizing margins provide a solid foundation for long-term value creation, even if multiple expansion remains constrained in the near term. This combination makes the stock an attractive anchor for investors seeking stability and defensive exposure, though not a compelling opportunity for outsized gains in the short run.